Atradius Atrium

Uusi online-palvelumme Atrium tarjoaa helpon pääsyn sopimustietoihin ja luottolimiittien hakuun.

Suomi

Suomi

Alankomaat

Alankomaat

Australia

Australia

Belgia

Belgia

Bulgaria

Bulgaria

Hongkongin SAR

Hongkongin SAR

Intia

Intia

Irlanti

Irlanti

Iso-Britannia

Iso-Britannia

Italia

Italia

Itävalta

Itävalta

Japani

Japani

Kanada

Kanada

Kiina

Kiina

Kreikka

Kreikka

Liettua

Liettua

Meksiko

Meksiko

Norja

Norja

Puola

Puola

Ranska

Ranska

Romania

Romania

Ruotsi

Ruotsi

Saksa

Saksa

Singapore

Singapore

Slovakia

Suomi

Slovakia

Suomi

Sveitsi

Sveitsi

Tanska

Tanska

Tšekki

Tšekki

Turkki

Turkki

Unkari

Unkari

Uusi-Seelanti

Uusi-Seelanti

Yhdysvallat

Yhdysvallat

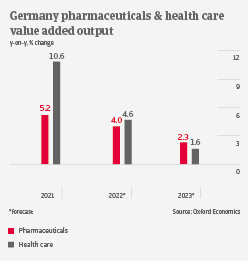

In 2020, Germany accounted for 4.5% of global pharmaceuticals production. Pharmaceuticals value added output is forecast to grow by 4% in 2022 and by more than 2% in 2023, after increasing 5.2% in 2021. Health care growth remains robust this year, expected to increase by more than 4%.

In 2020, Germany accounted for 4.5% of global pharmaceuticals production. Pharmaceuticals value added output is forecast to grow by 4% in 2022 and by more than 2% in 2023, after increasing 5.2% in 2021. Health care growth remains robust this year, expected to increase by more than 4%.

Covid-19 vaccines have mainly driven demand, while at the same time producers of cold medicines have recorded lower sales, as physical distancing and mask wearing reduced the number of related diseases. There is still a backlog of non-Covid related medical treatments and spending on drugs. However, a rebound is underway, and non-Covid related pharmaceuticals output will benefit this year and in 2023.

Mid-and long-term demand for pharmaceuticals will be driven by demographic developments. The progressive ageing of Germany´s population will require an increase in medical treatments, in particular for chronic diseases. This will mainly benefit producers of speciality products, but also manufacturers of generic drugs. The German healthcare market is highly regulated, and the legislative pressure on pharmaceutical businesses to lower their sales prices of drugs for end-consumers is not overly high.

Profit margins of both producers and pharmacies have increased in 2021, while pharmaceutical wholesalers/distributors continue to work with low margins. With a potential abatement or even an end of the pandemic we expect profit margins of producers and pharmacies will likely flatten.

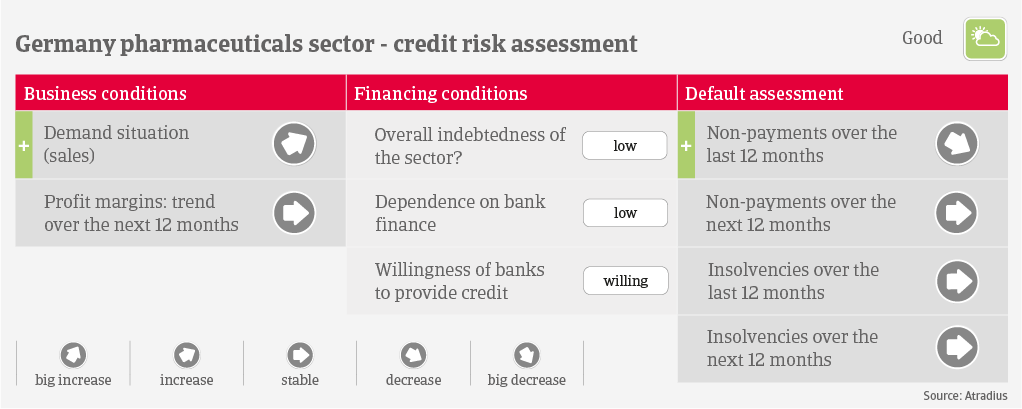

In general, German pharmaceutical businesses have robust equity, solvency and liquidity. Payments take 30-60 days on average. Compared with other German industries, the sector´s payment behaviour has always been better than average, with no notable payment delays. The insolvency environment is stable, and we expect business failures to remain at a low level. Due to the benign credit risk situation of most businesses and the good growth prospects in the coming years, our underwriting stance is open for producers, wholesalers/distributors and pharmacies/drugstores.