Atradius Atrium

Uusi online-palvelumme Atrium tarjoaa helpon pääsyn sopimustietoihin ja luottolimiittien hakuun.

Suomi

Suomi

Alankomaat

Alankomaat

Australia

Australia

Belgia

Belgia

Bulgaria

Bulgaria

Hongkongin SAR

Hongkongin SAR

Intia

Intia

Irlanti

Irlanti

Iso-Britannia

Iso-Britannia

Italia

Italia

Itävalta

Itävalta

Japani

Japani

Kanada

Kanada

Kiina

Kiina

Kreikka

Kreikka

Meksiko

Meksiko

Norja

Norja

Puola

Puola

Ranska

Ranska

Romania

Romania

Ruotsi

Ruotsi

Saksa

Saksa

Singapore

Singapore

Slovakia

Suomi

Slovakia

Suomi

Sveitsi

Sveitsi

Tanska

Tanska

Tšekki

Tšekki

Turkki

Turkki

Unkari

Unkari

Uusi-Seelanti

Uusi-Seelanti

Yhdysvallat

Yhdysvallat

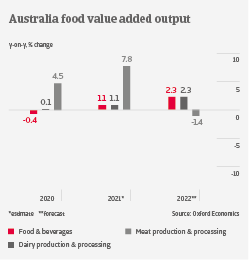

Australian food & beverages value added output is forecast to grow by more than 2% in 2022, after a 1.1% increase in 2021. The outlook is positive due to the easing of pandemic-related restrictions and ongoing overseas demand.

Australian food & beverages value added output is forecast to grow by more than 2% in 2022, after a 1.1% increase in 2021. The outlook is positive due to the easing of pandemic-related restrictions and ongoing overseas demand.

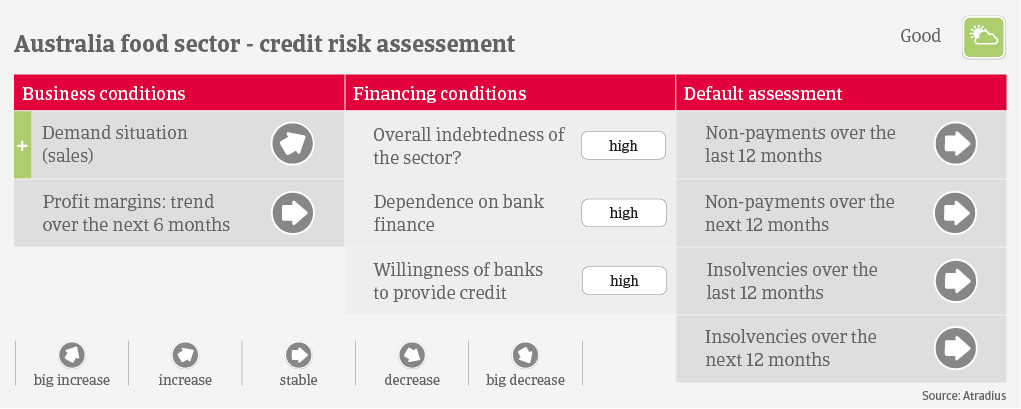

Conditions for food producers and processors are sound, supported by benign weather conditions (forecast of continued rainfall). Many food businesses are established players, and across all segments, the bulk of middle-sized companies is financially resilient, which should enable them to cope with ongoing challenges.

A container shortage currently affects exporters, in particular in the beverages segment. While larger businesses can cope with this issue, smaller players with lower margins could suffer should the shortage last. While sharply increased fertilizer prices affect grain producers and wholesalers, at the same time they benefit from robust output and higher sales prices. Consequently, grain and meat processors are facing higher input costs. Additionally, the meat segment has to cope with a cattle shortage after a decline in 2017-2019 caused by draught. The dairy subsector performs well, due to strong and established businesses in the market and higher milk prices.

While higher commodity and/or energy costs will surely have an impact on the margins of producers and processors, we do not expect a severe deterioration. Payments in the industry take 14 days on average, and the amount of both payment delays and insolvencies was historically low in 2020 and 2021, as businesses benefited from government support measures. We expect that the expiry of stimulus will trigger an increase in payment delays and insolvencies in 2022, mainly affecting food services businesses with weak liquidity and heavy gearing. Competition in this segment is high due to low entry barriers, and it has suffered from low hospitality and catering demand during the pandemic.

While we expect more food insolvencies in 2022 compared to 2019, this rise should be much lower than the increase of about 30% we forecast for all Australian businesses. Given the good or stable credit risk situation in all main subsectors apart from food services, our underwriting stance for the industry is generally open.