Atradius Atrium

Uusi online-palvelumme Atrium tarjoaa helpon pääsyn sopimustietoihin ja luottolimiittien hakuun.

Suomi

Suomi

Alankomaat

Alankomaat

Australia

Australia

Belgia

Belgia

Bulgaria

Bulgaria

Hongkongin SAR

Hongkongin SAR

Intia

Intia

Irlanti

Irlanti

Iso-Britannia

Iso-Britannia

Italia

Italia

Itävalta

Itävalta

Japani

Japani

Kanada

Kanada

Kiina

Kiina

Kreikka

Kreikka

Liettua

Liettua

Meksiko

Meksiko

Norja

Norja

Puola

Puola

Ranska

Ranska

Romania

Romania

Ruotsi

Ruotsi

Saksa

Saksa

Singapore

Singapore

Slovakia

Suomi

Slovakia

Suomi

Sveitsi

Sveitsi

Tanska

Tanska

Tšekki

Tšekki

Turkki

Turkki

Unkari

Unkari

Uusi-Seelanti

Uusi-Seelanti

Yhdysvallat

Yhdysvallat

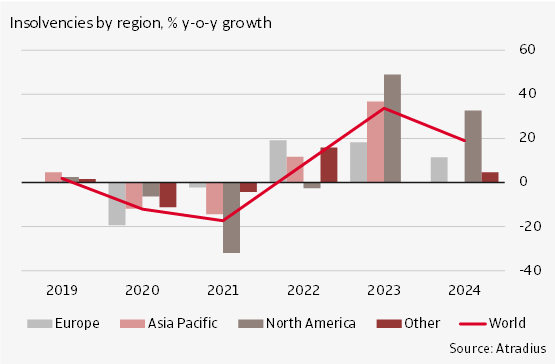

The insolvencies adjustment process, which was already initiated in 2022, is continuing at an accelerated pace in 2023. The phasing out of fiscal support measures and the lifting of temporary changes to insolvency legislation have had an effect on the level of insolvencies. After a global increase of 9% in 2022, we expect a 34% increase in in 2023. We are seeing rising insolvencies across all regions, with North America experiencing a relatively strong increase, while Europe is seeing milder increases. The majority of countries in each region can expect rising insolvencies this year. In 2024, the picture is more mixed. While we still expect an increase for most markets, the percentage increase is lower than in 2023. On a global level, we predict that insolvencies in 2024 rise by 19% compared to 2023. By the end of 2024 insolvencies are expected to have more or less normalised compared to pre-pandemic levels.

The world economy is gradually losing steam as the effects of past monetary tightening and China’s slowdown take hold. We now forecast world GDP to grow 2.5% this year. Forward-looking sentiment indicators point to a more significant slowdown in the second half of 2023. The global services PMI, which has been soaring on the back of post-pandemic demand surplus, has declined in August for the third month in a row. Inflation pressures are easing, but it is too early to declare victory on inflation. Major central banks, including in Europe and the US, are expected to keep policy rates at current levels until 2024. For 2024, we foresee a slightly lower growth rate of 2.0%.

Growth in emerging markets is likely to remain weak by historical standards. We expect GDP growth to stay in lower gear at 4.0% this year and 3.7% in 2024, as weak external demand and tightening global financing conditions keep a lid on growth. Under the headline figure lies substantial heterogeneity. Emerging Asia remains the fastest growing region this year (5.2%). We forecast Chinese GDP to grow by 5.1%, which is higher than expected six months ago, as the earlier than expected abandoning of Covid lockdowns led to a front-loading of private consumption during the reopening process. But consumption made much less of a contribution to GDP growth in Q2 of 2023. Furthermore, weakness across the property sector remains, with negative spillovers to other segments of the economy. This is slowing GDP growth into 2024 (4.6%). In Eastern Europe, the outlook continues to be dominated by the Russia-Ukraine war. Despite massive Western sanctions, Russia is still able to export large amounts of oil, which underpins economic growth. GDP growth is forecast to be 2.4% in 2023 and 1.2% in 2024. In Turkey, the new government is showing a willingness to move towards more orthodox policymaking. Since the presidential elections, the lira has depreciated to a new record low. While fuelling inflation in the near term, it is also partly good news as it shows a willingness by the authorities to bring the currency more in line with its underlying value.

Growth in advanced economies is just 1.4% in 2023, followed by 0.6% in 2024. The United States economy expanded at a solid pace in Q2, driven by solid consumer spending and a tight labour market. However, we expect the growth slowdown to continue and a mild recession in Q4 and into Q1 2024. The downturn will be driven by the impact of central bank policy rate hikes, tighter lending conditions and high inflation leading consumers and business to cut back on spending and investment. In the eurozone, GDP expanded by 0.3% in Q2, but the around half of this increase was driven by a rebound in Ireland due to transactions of multinational companies that influence the GDP figures. We believe economic activity in the eurozone will be subdued in the second half of 2023, driven by continued weakness in the manufacturing sector and weaker external demand as global growth is slowing. We forecast a relatively subdued growth both in 2023 (0.5%) and 2024 (0.9%).

Policy tightening by central banks created a brief banking scare in March 2023, leading to the forced takeover of Credit Suisse in Switzerland and the bankruptcy of several US regional banks. Immediate concerns about the banking sector have subsided, but the central bank tightening is filtering through the financial system, leading to a tightening of lending standards. Bank lending surveys in the United States and Europe suggest that banks restricted access to credit considerably in Q2 of 2023, and they are expected to continue to do so in coming months. The tightening of financial conditions in advanced markets also has spillover effects to emerging markets. Several emerging markets have experienced sharp currency depreciations since the Federal Reserve started to increase interest rates. On the fiscal side, the overall fiscal position of major advanced economies continues to be expansionary, bus less expansionary than during the pandemic. Several countries have adopted support packages to counter the negative effects of the rise in energy prices, which gives some support to economic growth. However, with energy prices falling, such a fiscal stimulus will be less necessary. We project fiscal adjustment to take place in advanced and emerging economies in 2024.

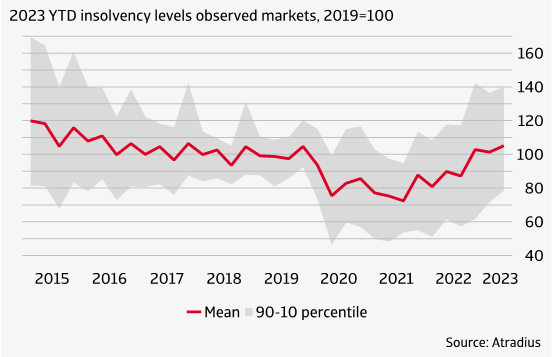

The global number of insolvencies increased by 9% in 2022 as the pandemic support packages and temporary changes to insolvency legalisation were lifted. Chart 1 gives the year-to-date insolvencies index in 2023 relative to 2019. A value above 100 indicates that the insolvency level is above the (pre-pandemic) 2019 level. A value below 100 means the insolvency level is still lower than in 2019.

As becomes clear from Chart 1, the mean insolvency level in 2023 Q2 was already above the 2019 level. The grey area (90-10 percentile) indicates that the spread of the insolvency level is still wide across countries. Some markets are well above the pre-pandemic level, while others are still in the process of adjustment. We consider a market to have adjusted fully back to ‘normal’ if the index value is at least 95%. Subject to a couple of data changes (see Box 1), currently 17 out of 29 observed markets have adjusted fully back to normal or are even overshooting the pre-pandemic insolvency levels. Six months ago this was the case for 12 markets. Therefore, at this moment only in a minority of markets the adjustment back to normal is still underway.

box 1. data changes |

|---|

|

Compared to our March 2023 Insolvency Forecast report, in this edition we implemented some changes in the data underlying the headline insolvency counts for New Zealand, Spain and South Korea. For South Korea, we previously used the number of defaults on commercial paper as reported by the Bank of South Korea as part of the ‘Dishonored Bill Ratio’ release. One problem with this source is that it captures only a narrow definition of defaults, as commercial paper is used only by larger corporations. Another problem is that the defaults, together with the underlying cleared bills, had a pronounced downward trend which indicated that the use of this instrument was decreasing. Therefore, we decided to replace the dishonoured bill ratio series with the bankruptcy filings reported by the Supreme Court of Korea. This latter series has the advantage that it has a broader scope, in line with the definition of bankruptcies that we are using for other markets. Moreover, the dynamics of the series matches our expectations, with a decrease in the number of defaults during 2021 that can be attributed to the Covid government intervention and a normalization in 2023. For New Zealand, we noticed that the series we used as headline series for insolvencies was associated with personal insolvencies and that our source, the Official Assignee’s Office, was processing only a part of the total insolvency cases. Therefore, we decided to use instead as a source the corporate insolvencies reported by the New Zealand’s Companies Register that captures all the insolvencies that were placed into liquidation, receiverships and voluntary administrations. For Spain we found that a legislation change starting in 2022Q4 affected the continuity of the insolvency statistics reported by our source, the Official College of Property & Mercantile Registrars of Spain. More specifically, the statistics starting from 2022Q4 cannot differentiate anymore between persons with business activity and without. Therefore, we decided to take out personal insolvencies from our headline aggregate. This implies important historical revisions as persons with business activity comprised of a significant share in our headline insolvencies counts (28% in 2022Q3). Another change compared to the previous Insolvency Forecast report is that we decided to stop publishing forecasts on Russian insolvencies. The economic situation in Russia is very unpredictable and we had some doubts about the reliability of the data even before the conflict with Ukraine. |

We now turn to our insolvency forecast for 2023 and 2024, which is given in year-on-year % changes (e.g. 2023 compared with 2022). On a global level, we predict that insolvencies increase by 34% year-on-year in 2023 (Chart 2). On a regional level, we foresee a relatively strong increase of insolvencies in North America (49%), which is mainly driven by the United States. For Europe, we expect a somewhat smaller increase of 18% as the process of normalisation of insolvencies in Europe is more advanced compared to other regions. For Asia Pacific we predict an increase of 37%. In 2024, North America remains the region with the highest insolvency growth (33%), while development is flatter in the other regions.

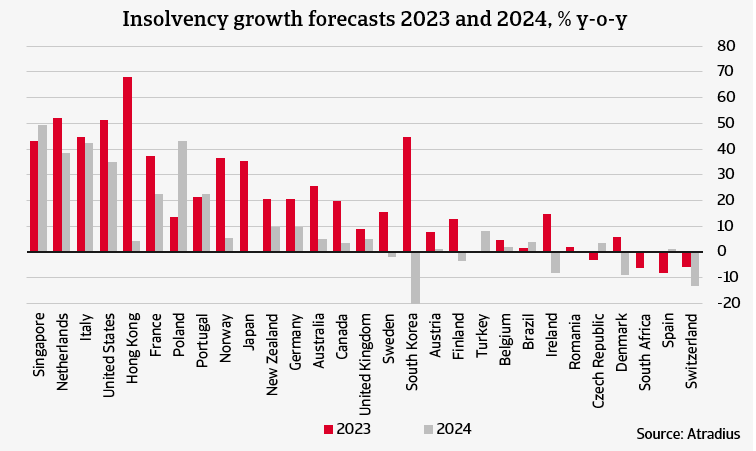

Chart 3 presents our insolvency forecast for 2023 and 2024 on a country level. The markets are arranged in the order of cumulative insolvency growth over the 2023-2024 period. The highest insolvency growth rates in 2023 are recorded in Hong Kong, the Netherlands, the United States, South Korea and Italy. For the Netherlands, the United States and Italy, insolvencies were relatively low at the start of 2023 and the projected insolvency growth in 2023 is mostly driven by an adjustment back to pre-pandemic levels. For South Korea and Hong Kong, the increase in insolvencies was already well underway in 2022. In Hong Kong, there is still some return to normal in 2023, but also a significant upward effect from zombie companies going bankrupt. For South Korea, the increase that was already visible last year continued in the first half of 2023, which pushes up the insolvency growth in the full year.

There are also markets with relatively low or negative insolvency growth in 2023. Countries for which we expect a decline in insolvencies in 2023 are Spain, South Africa, Switzerland and Czech Republic. In Spain, Switzerland and Czech Republic the insolvency level has increased throughout 2022 to above the normality level, in part due to the assumed bankruptcy of zombie firms. In 2023, we forecast a decline, such that the insolvency level moves closer to the normality level. For South Africa we saw a decrease of insolvencies in the first half of 2023 that is a bit hard to interpret given the challenging economic situation. Countries for which we expect relatively mild insolvency growth include several European countries where insolvencies have already normalised in 2022, including Denmark, Belgium and Austria.

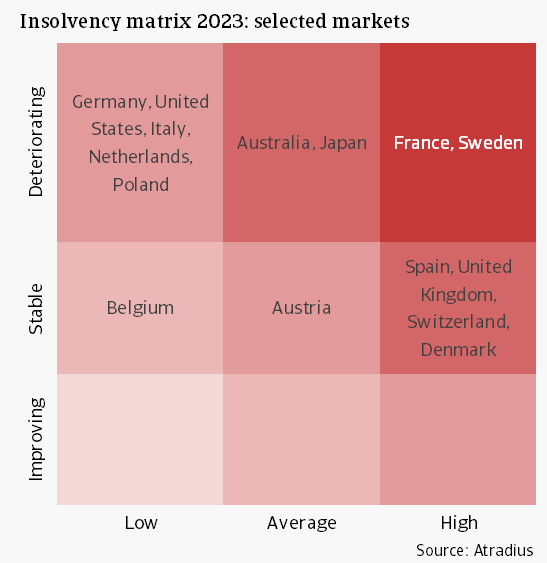

Chart 4 shows the insolvency developments across another dimension. The vertical axis of the insolvency matrix shows the year-on-year expected change of insolvencies in 2023 compared to 2022. Insolvency growth considered ‘deteriorating’ if growth is higher than 10%, ‘stable’ if it is between -10% and +10%, and ‘improving’ if it is lower than -10%. The horizontal axis shows the level of insolvencies in 2023 compared to 2019. This gives a better impression how the current level of insolvencies compares to the pre-pandemic level. We identify the level as ‘high’ if in 2023 it is expected to be above 105% of the 2019 level, ‘average’ if it is between 95% and 105%, and ‘low’ if it is below 95%.

There are several countries with a stable insolvency situation, i.e. countries that see an insolvency change between -10% and +10% in 2023. These include Belgium, Austria, Spain, the United Kingdom, Switzerland and Denmark. Among these countries, the UK is an interesting market, as the insolvency level is relatively high: 140% of the pre-pandemic level. The majority of countries, however, see a tendency for bankruptcies to deteriorate in 2023, even though the level compared to pre-pandemic often remains ‘low’. France and Sweden are two examples of countries in a more worrisome position, as the situation in 2023 is ‘deteriorating’, while the insolvency level in 2023 is also considered ‘high’.

For 2024 we are still predicting insolvency increases for the majority of markets, but the percentage increase is generally lower than in 2023. On a global level, we predict that insolvencies rise by 19% compared to 2023. We see a substantial increase in insolvencies in a number of countries. In Singapore, Poland, Italy, the Netherlands and the United States the normalization started in late 2022 or early 2023 and we expect that this will continue well into 2024. For Poland and Italy we did not see yet the normalization starting, but we have no reason to believe that this will not occur similarly in the second half of 2023 and 2024.

In contrast, for a significant number of markets, we think that insolvencies will again start to decline or remain approximately constant. This is because insolvency levels will have largely returned to normal and zombie firms that are not able to survive without support, have gone bankrupt already in 2023.

Countries with a negative expected insolvency growth in 2024 are, for example, South Korea, Switzerland, Denmark and Ireland. In Switzerland, 2024 brings another year of decrease in insolvencies, as the insolvency level continues to move to a normality level that is comparable with the 2019 level. In South Korea, Ireland and Denmark, the relatively high level of insolvencies of 2023 is expected to be reversed in 2024.

The coming years are likely to remain challenging for firms. Companies were able to rebuild cash buffers since the pandemic, but lately these are under pressure due to squeezed profit margins and tightening funding conditions. They emerged from the pandemic with much higher debt. The ability to service this debt is an increasing challenge in an environment with higher interest rates. Financial markets are increasingly taking into account that central banks will not ease for the time being, which will have consequences for companies' financing conditions. For emerging markets, there is the added challenge that a depreciation of the currency will push up corporate borrowing costs even further.

Theo Smid, Senior Economist

theo.smid@atradius.com

+31 20 553 2169

Iulian Ciobica, Economist

iulian.ciobica@atradius.com

+31 20 553 2121

All content on this page is subject to our Disclaimer, available here.